By Jen Saarbach & Kristen Kelly, Co-Founders of The Wall Street Skinny

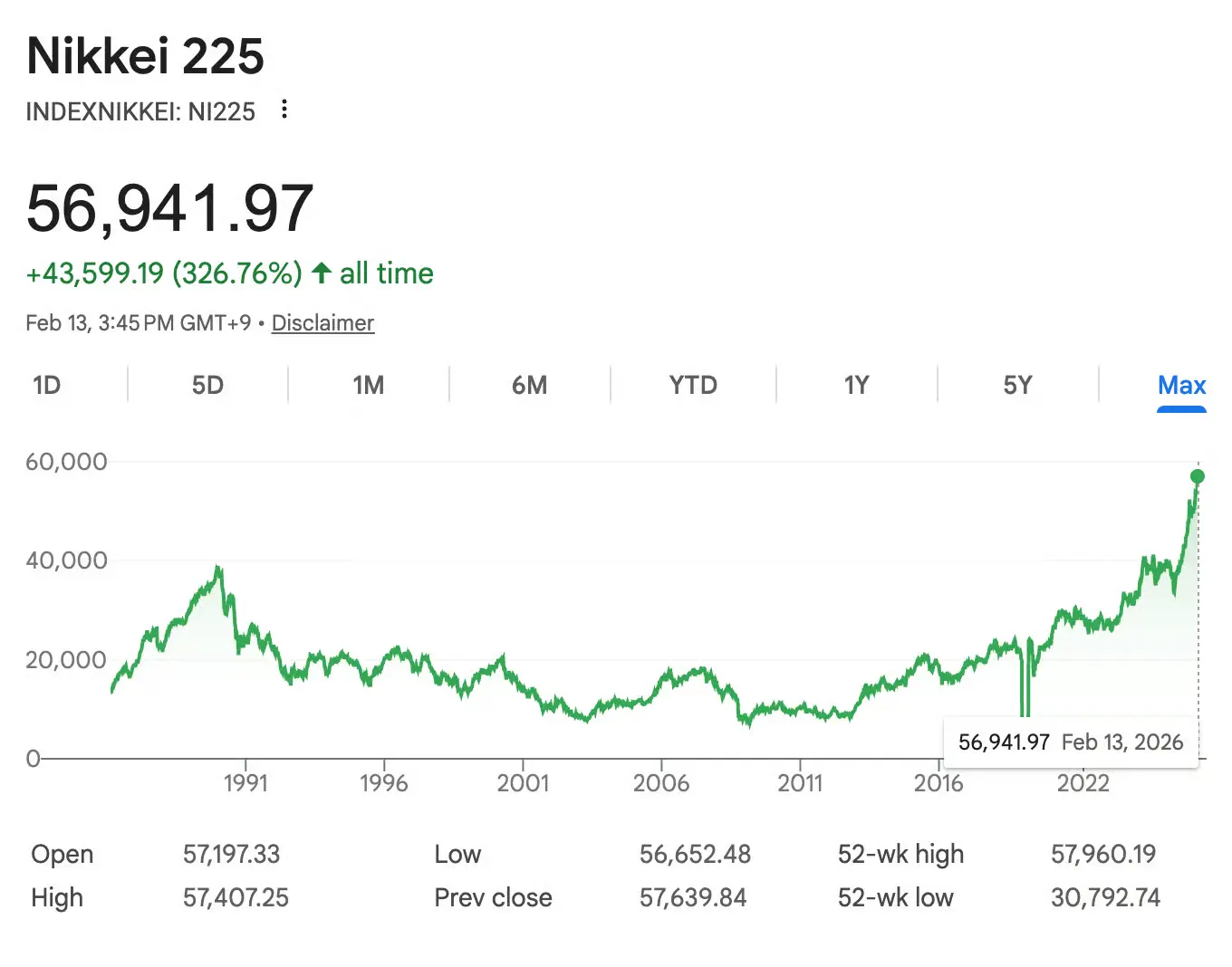

Japan’s stock market hasn’t been here since the bubble economy of the late 1980s. The Nikkei 225 and TOPIX have both surged to record highs, closing a chapter that investors called “three lost decades.”

But this isn’t a single-catalyst story. It’s the payoff of a reform arc that began over a decade ago with Shinzo Abe.

When Shinzo Abe became Prime Minister in late 2012, Japan was trapped in a deflationary spiral. His response was a sweeping economic program, “Abenomics,” built on three “arrows”:

- Monetary easing: Massive QE, negative rates, yield curve control

- Fiscal stimulus: Infrastructure & cash injections

- Structural reform: Corporate governance, tax cuts, labor flexibility

The first two made headlines, with massive bond purchases and government spending. But it’s the third arrow, particularly corporate governance reform, that is less-discussed and is our focus today.

A system built for safety, not shareholders

For decades, Japanese corporations were run for employees and stability, not shareholders. Companies sat in keiretsu networks – corporate groups holding each other’s shares, hoarding cash and prioritizing employee well being over returns. Boards were dominated by insiders. CEOs were rarely removed for underperformance. Nearly 43% of listed companies traded below book value.

That model worked in the postwar boom, but it became a drag during three lost decades of deflation.

Demographics forced the issue

Japan has an inverted population pyramid: a shrinking workforce supporting an ever-growing number of retirees. Over 28% of the population is 65+. By 2050, there will be just 1.2 workers per retiree. Japan has one of the world’s largest pension funds (GPIF, with $1.87 trillion in assets), which recently adjusted their portfolio and doubled their equity allocation to 50%, with a bias for domestic equities. But, here’s the thing. You need those stocks to actually perform in order to create value. That’s where corporate governance comes in.

Inflation changed everything

Now add inflation. For the first time in 30+ years, Japan has sustained price increases closing in on 2%. Unlike how we currently perceive inflation in the US, for a country like Japan that fought deflation for decades, this is a good thing.

Companies can raise prices for the first time in a generation. Workers are getting real wage increases. Households are moving savings into equities; ¥7.5 trillion flowed into investment accounts in just the first half of 2024. And companies can no longer justify hoarding cash. Uninvested capital now loses real value every year.

Enter Sanae Takaichi

In October 2025, Sanae Takaichi became Japan’s first female PM. She also won a historic supermajority in the February 8th snap elections, giving her the strongest mandate any Japanese PM has held in decades. As Abe’s protégée, she’s doubling down on his playbook. Her economic program, “Sanaenomics,” favors expansionary fiscal policy and strategic investment in sectors like semiconductors, AI, and defense.

The Tokyo Stock Exchange is naming and shaming companies that don’t improve capital efficiency. Buffett is buying Japanese stocks. It’s all converging.

The bottom line

Ultimately, this isn’t a momentum trade or a single-catalyst pop. It’s the culmination of a decade-long structural shift from a market that prioritized stability over returns to one that’s finally being rewired to increase shareholder value.